Case Study

ExxonMobil Proxy Battle in May 2021

Written by team at Act Analytics On June 11, 2021

8 min read

8 min read

On Wednesday, May 26th, 2021, there were a number of events that will accelerate energy company responses to climate change. One of these was activist hedge fund Engine No. 1 managing to secure two seats on Exxon-Mobil’s board. The two new board members were nominated to drive the firm to respond more proactively in mitigating climate change by reducing carbon emission to net zero by 2050. This outcome represents a major win for environmentally-concerned investors. Exxon’s CEO, Darren Woods, opposed the nominees.

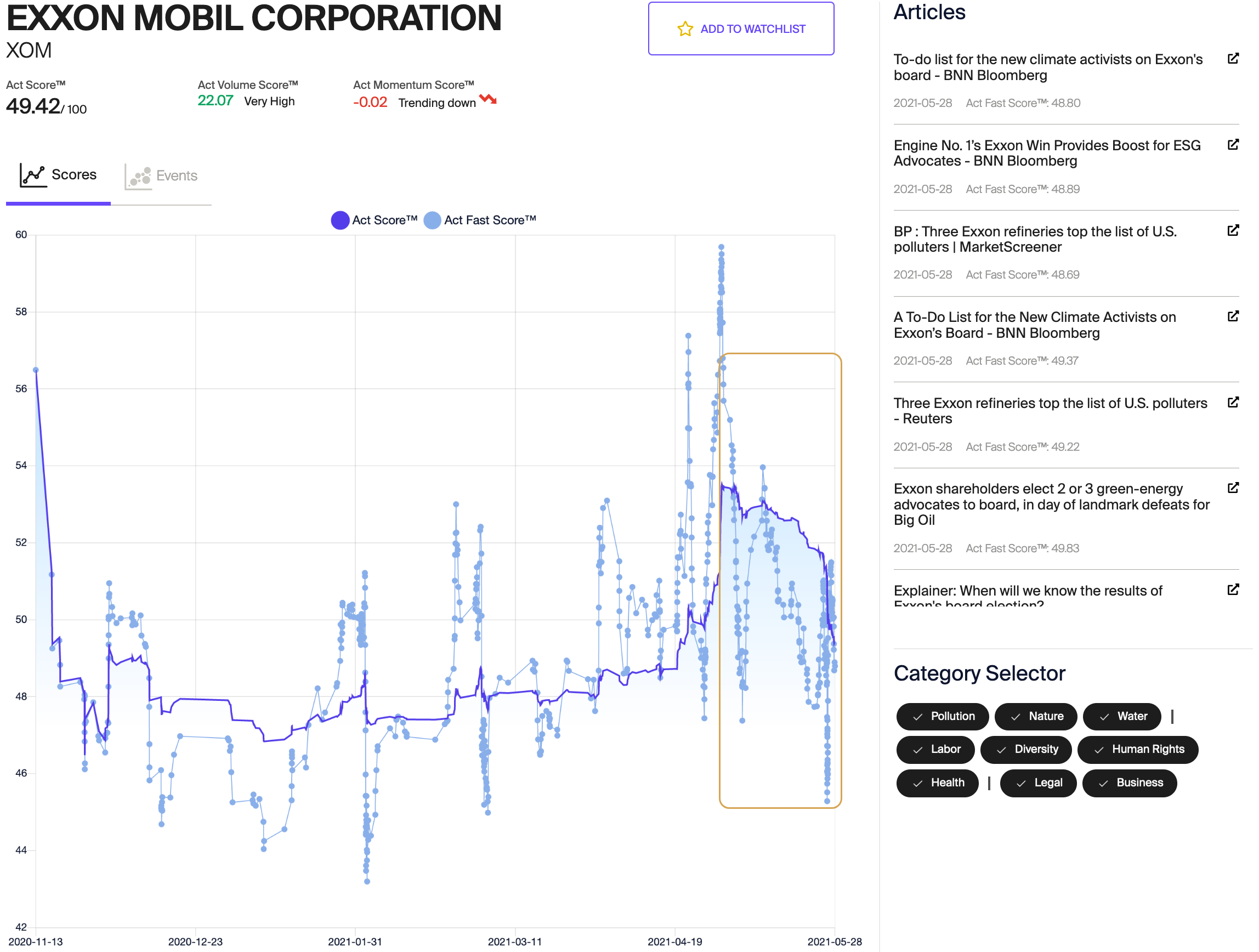

The interesting story is how the news events leading up to the vote emerged and expanded and, subsequently, the equity market response. Engine No. 1 filed its proxy statement with the SEC on March 11th, 2021. This event was covered in the news but did not get a great deal of attention. As the board vote approached, the story grew. On May 4th, Reuters reported that the Sierra Club and other environmental groups were lobbying BlackRock and Vanguard, which together own more than 13% of XOM shares, to vote to support board members proposed by Engine No. 1. On May 11th, Britain’s largest asset manager announced that it would back Engine No. 1’s slate of director nominees. On May 12th, Pensions and Investment Research, a major proxy voting advisor, endorsed the four Engine No. 1 board nominees. On May 14th, Institutional Shareholder Services (ISS), another major proxy voting advisor, announced that it backed three out of four of Engine No. 1’s nominees. The Act Score dropped continuously through May.

In analyzing returns for XOM, we identified a three day run of anomalous negative returns from May 18th through May 20th (after correcting for beta effects relative to the S&P 500) over which XOM fell 5.39% and the S&P 500 rose by 0.06%. This 3-day negative return anomaly (three successive days in which the return of XOM was less than would be predicted using the stock’s beta and each day’s S&P 500 return) is the second-largest negative return anomaly in the past 90 days and the third-largest in the last six months. A notable feature of this decline in XOM, in both absolute terms and relative to the broader market, is that it occurred well before the actual board vote. After this decline, the share price was quite stable until the vote. The cumulative return for XOM for the period from May 21st through May 26th was 0.17%, as compared to 0.91% for the S&P 500. For May of 2021, XOM’s total return is 3.49% vs. 5.74% for the Integrated Oil and Gas sector. The Energy Select Sector SPDR (XLE), in which XOM is the largest holding, returned 5.7% for the month.

While there is no way to definitively establish a causal link between the evolution of the news on the board vote and the idiosyncratic decline in Exxon’s share price, the major news stories about the gathering momentum in support of Engine No. 1’s proposals in the first weeks of May (reflected in the decline in the Act Scores) and the subsequent price decline are suggestive.

Discussion

Having the Act Analytics scores declining as a result of the efforts of environmentally-focused activist investors may seem counter-intuitive. Our interpretation is that the falling Act scores leading up to the board vote reflect the conflict between activist investors and the XOM’s CEO and the pre-vote board, rather than a negative view of Engine No. 1’s agenda. The increasing traction for replacing board members was positive news for ESG investors, but strife at the board level is typically not good news for a company.

Looking at the Act Analytics scores for XOM in the two weeks leading up to the vote shows a progressive decline in sentiment pertaining to XOM’s upcoming board vote from early to mid-May, followed by a 5.4% decline in Exxon’s share price over a 3-day period through May 20th, during which the S&P 500 was flat. XOM shares were then essentially flat from May 21st until May 26th, when the results of the vote were announced. The market responded to the emerging news well before the actual vote. Similar to other cases that we have observed, the news stories on the board battle needed to fully emerge, with new details fleshed out, before the market responded. We conceptualize this transition as a news tipping point. Before the tipping point is reached, the market does not collectively incorporate a specific event or series of events. Once a critical level of dissemination is reached, prices adjust.

One of the uses of news-based sentiment scores is to assist investor relations (IR) groups in assessing how relevant events impact overall perception of a company. In this case, the Act Scores showed a continuous decline in XOM’s overall rating as support for Engine No. 1 grew, foreshadowing the outcome of the vote.

This case has implications for ESG investors and portfolio managers. First, shareholder activism to make companies better corporate citizens may, in the near term, reduce the firm’s overall sentiment-based ratings when senior management opposes these changes. This conflict may also drive reduced share valuations. In this case, ESG investors would have been well-served to sell holdings in XOM because of the firm’s reluctance to accelerate decarbonization. The Act Analytics score declines provided an alert to the conflict between a growing group of institutional investors and Exxon’s senior management. The market responded with a reduction in Exxon’s share price ahead of the board vote.

Download PDF- Real time ESG intelligence

- 4 King St. West Suite 1060, Toronto, Ontario

- Tel +1 647 200 6482

- info@act-analytics.com