Case Study

Characterizing Significant News Events for Boeing Stock

Written by team at Act Analytics On August 2, 2021

15 min read

15 min read

Introducing the Act Event Classification

One of the largest challenges for money managers is determining which news events are likely to impact a stock’s valuation, which contain information that is already priced into the shares, and which are not important. Act Analytics uses Natural Language Processing (NLP) to aggregate ESG news about a company and assess close to real-time whether the news is positive or negative. The NLP analysis can include up to nine thematic categories on which to filter and analyze results.

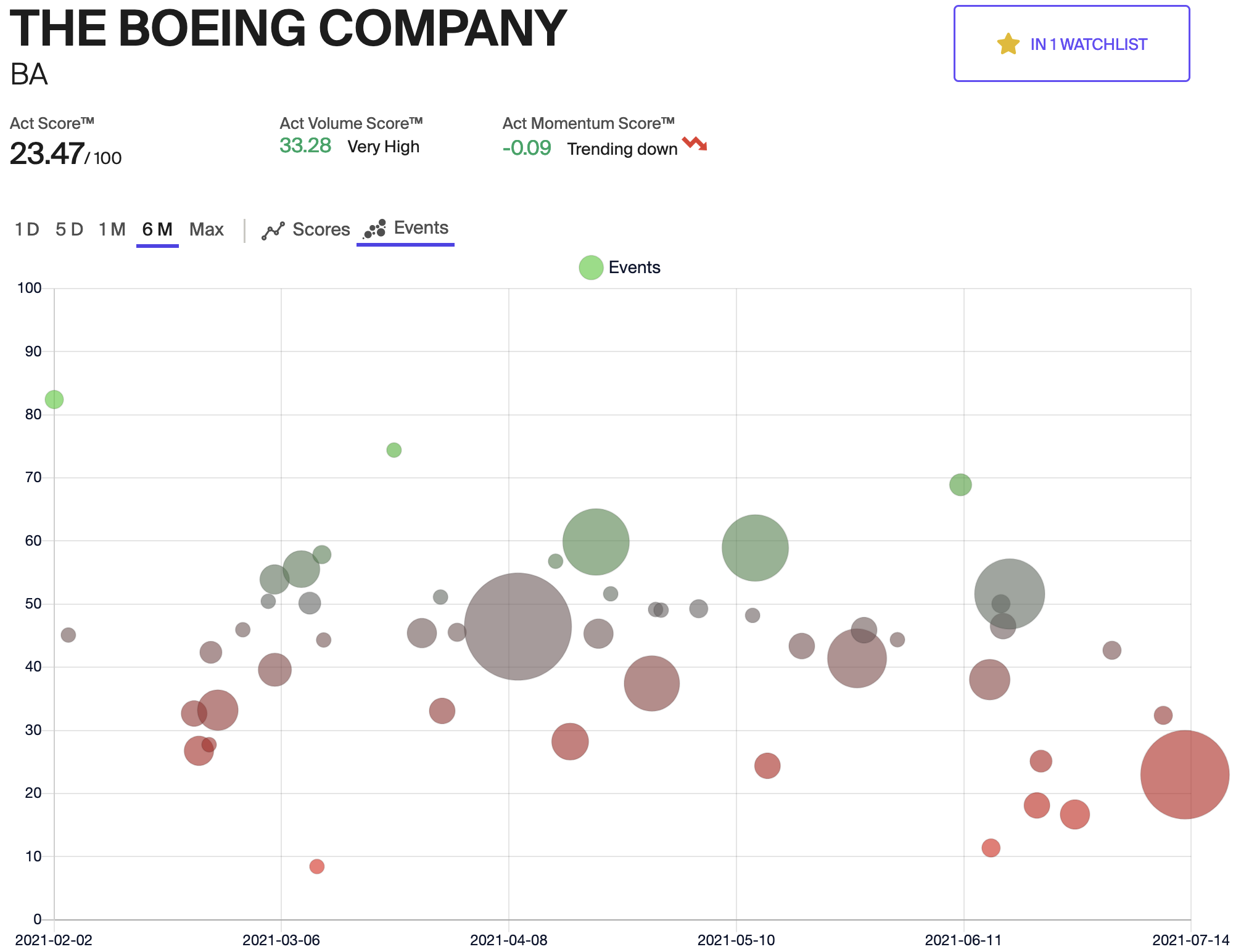

Act Analytics has recently introduced functionality using intelligent clustering algorithms that combines news stories into ‘events’ or clusters that are about the same underlying event or situation. In this case study, we provide an example of event analysis for Boeing (BA), along with initial findings that suggest that the Act Event Score may provide value in predicting whether news events are likely to drive a positive or negative market response. We have included all nine categories of news for the purposes of this case study.

News articles for a stock are aggregated into common clusters around semantic similarity and which appear around the same time or in close temporal proximity to one another. Each of these events is plotted as a circle on the chart. The NLP algorithm assesses all of the news stories that are part of the event cluster, and calculates an aggregate score for the event (shown on the vertical axis of the chart above) along with a start and end date for the event (the earliest and most recent dates of news articles included in the event). The scores are normalized to range from 0 (most negative sentiment) to 100 (most positive sentiment). The color of the events indicates whether the news event is positive (green) or negative (red) for the company and the size of the circle is larger for events with a larger number of articles in the event.

Mapping News Events to Return Anomalies

To examine whether there is a relationship between news events and significant return anomalies, we start by ranking the largest magnitude price return anomalies (both positive and negative) for BA over the past six months. The procedure, described here, calculates the return for a stock after correcting for beta relative to the market index (the S&P 500 in this case). We then look at cumulative negative and positive anomalies over one or more days. If the return anomaly is negative on day 1, negative on day 2, and positive or zero on day 3, the firm two days comprise negative return anomaly, for example.

The next step is to determine whether there are news events that occur shortly before, or contemporaneously with, the start of a return anomaly. The ten largest positive and negative anomalies over the past six months to which we have mapped a news event for BA are shown in the tables below.

| Date Range of Event | # of Articles | Event Score | Cumulative Return Anomaly | End Date | Start Date | Length (Days) |

|---|---|---|---|---|---|---|

| From 2021-04-20 16:49 to 2021-04-21 01:07 | 8 | 45.33 | 2.29% | 4/27/2021 | 4/22/2021 | 4 |

| No event | 2.55% | 2/9/2021 | 2/8/2021 | 2 | ||

| No event | 2.56% | 3/25/2021 | 3/25/2021 | 1 | ||

| No event | 2.82% | 3/17/2021 | 3/17/2021 | 1 | ||

| From 2021-06-18 02:20 to 2021-06-18 23:52 | 19 | 51.62 | 2.91% | 6/21/2021 | 6/18/2021 | 2 |

| No event | 3.06% | 2/16/2021 | 2/16/2021 | 1 | ||

| From 2021-05-19 13:40 to 2021-05-21 13:17 | 7 | 43.36 | 3.26% | 5/21/2021 | 5/21/2021 | 1 |

| No event | 3.26% | 7/8/2021 | 7/8/2021 | 1 | ||

| From 2021-06-02 03:38 to 2021-06-02 14:38 | 4 | 44.36 | 3.38% | 6/2/2021 | 6/1/2021 | 2 |

| From 2021-05-27 10:08 to 2021-05-27 23:0 | 14 | 41.42 | 3.79% | 5/27/2021 | 5/27/2021 | 1 |

| From 2021-02-02 08:53 to 2021-02-02 20:13 | 5 | 82.42 | 3.82% | 2/4/2021 | 2/2/2021 | 3 |

| From 2021-03-28 06:26 to 2021-03-30 10:04 | 4 | 51.13 | 3.90% | 3/31/2021 | 3/29/2021 | 3 |

| No event | 4.55% | 2/19/2021 | 2/19/2021 | 1 | ||

| From 2021-02-24 14:44 to 2021-02-25 01:31 | 6 | 42.36 | 6.62% | 2/24/2021 | 2/24/2021 | 1 |

| From 2021-03-01 03:35 to 2021-03-01 06:32 | 4 | 45.94 | 7.42% | 3/4/2021 | 3/1/2021 | 4 |

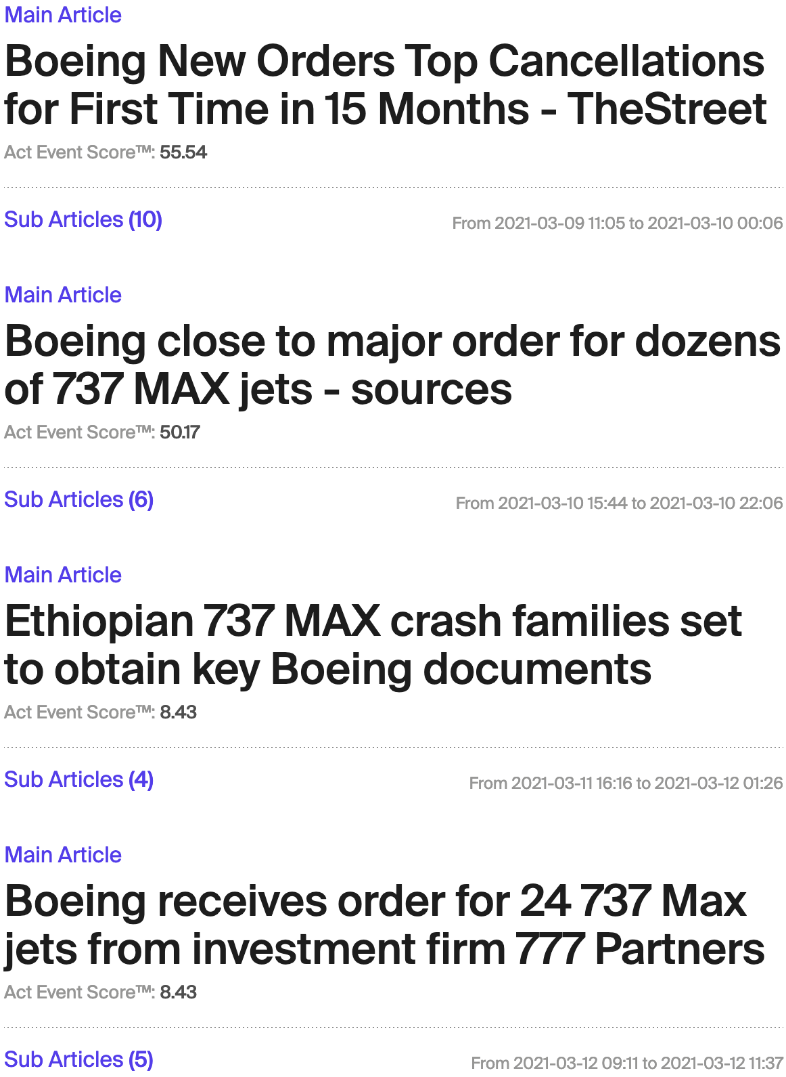

| From 2021-03-09 11:05 to 2021-03-10 00:06 | 10 | 55.54 | 16.38% | 3/12/2021 | 3/8/2021 | 5 |

| Date Range of Event | # of Articles | Event Score | Cumulative Return Anomaly | End Date | Start Date | Length (Days) |

|---|---|---|---|---|---|---|

| From 2021-03-26 14:58 to 2021-03-28 06:31 | 8 | 45.41 | -3.13% | 3/26/2021 | 3/26/2021 | 1 |

| From 2021-04-09 06:18 to 2021-04-09 23:26 | 29 | 46.43 | -3.16% | 4/12/2021 | 4/9/2021 | 2 |

| From 2021-03-05 16:49 to 2021-03-06 01:11 | 9 | 39.60 | -3.17% | 3/5/2021 | 3/5/2021 | 1 |

| No event | -3.46% | 2/18/2021 | 2/17/2021 | 2 | ||

| From 2021-04-28 06:45 to 2021-04-28 20:29 | 15 | 37.43 | -3.50% | 4/29/2021 | 4/28/2021 | 2 |

| From 2021-02-25 14:27 to 2021-02-26 00:14 | 11 | 33.20 | -3.66% | 2/26/2021 | 2/25/2021 | 2 |

| No event | -3.94% | 6/14/2021 | 6/9/2021 | 4 | ||

| From 2021-07-09 21:46 to 2021-07-10 01:11 | 5 | 32.38 | -5.01% | 7/13/2021 | 7/9/2021 | 3 |

| No event | -5.81% | 3/16/2021 | 3/15/2021 | 2 | ||

| From 2021-03-22 15:58 to 2021-03-22 18:56 | 4 | 74.41 | -5.83% | 3/24/2021 | 3/22/2021 | 3 |

| From 2021-01-18 09:59 to 2021-01-19 23:20 | 7 | 52.75 | -6.49% | 1/27/2021 | 1/20/2021 | 6 |

| From 2021-06-27 08:45 to 2021-06-27 22:07 | 8 | 16.68 | -6.71% | 6/29/2021 | 6/25/2021 | 3 |

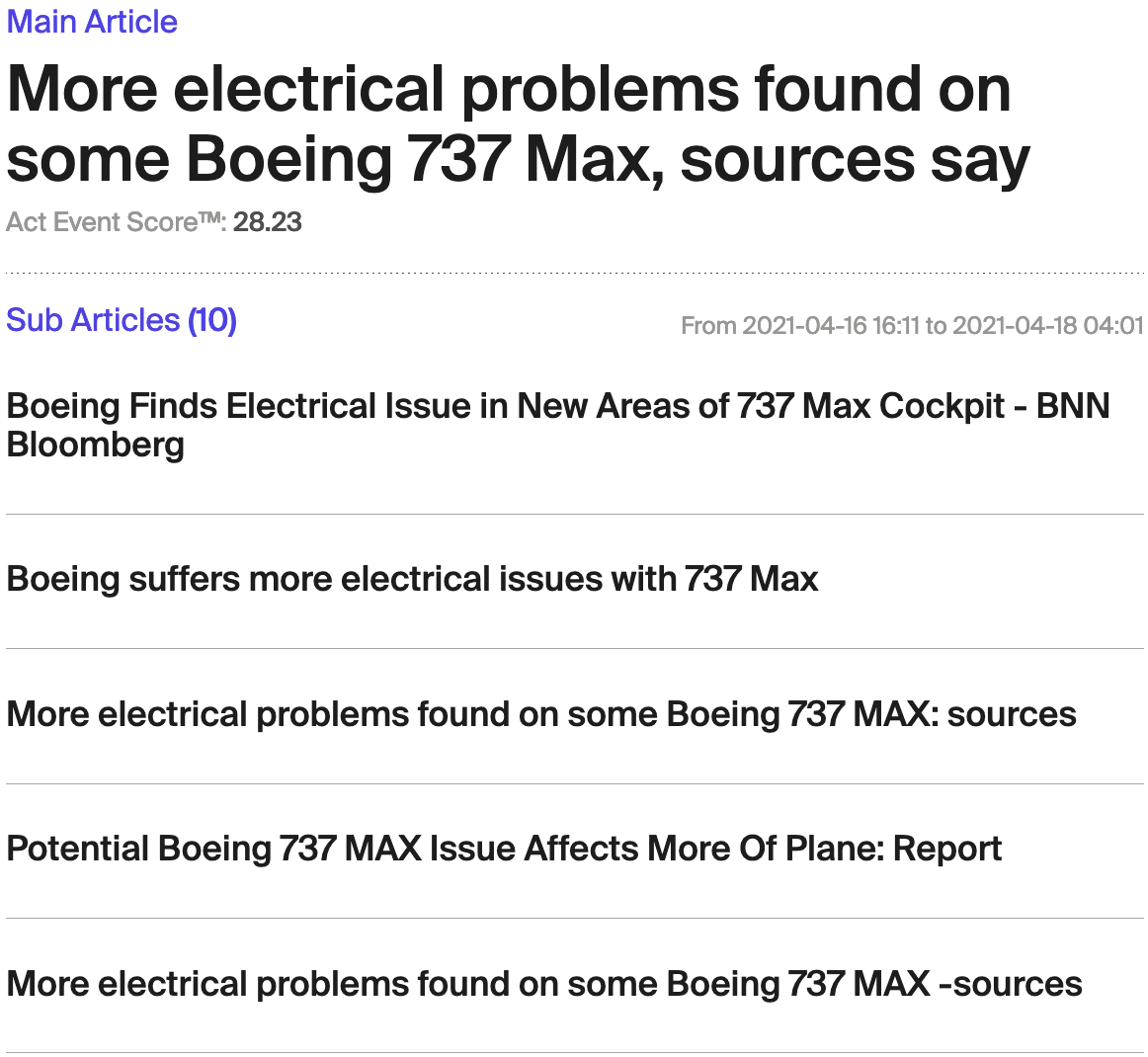

| From 2021-04-16 16:11 to 2021-04-18 04:01 | 10 | 28.23 | -7.95% | 4/21/2021 | 4/15/2021 | 5 |

The left half of the tables shows the properties of the news event identified by Act Analytics. The date range of event shows the starting and ending dates of articles in the event. The Event Score shows the aggregate Act Analytics score for the articles that are part of the event. The right side of the table shows the properties of the return anomalies over one or more days. The events are mapped to the return anomalies by identifying the news event that occurs close to the start of the return anomaly or that substantially overlaps the time period of the return anomaly. The Event Scores shown in this analysis are based on all ESG categories, but could be analyzed at a more granular level e.g. pollution or legal risk to identify patterns.

There are different types of event / return anomaly pairs. In the first, a news event occurs and then the market response plays out over one or more days. In this situation, the news event may occur on the same calendar day as the market response. In the second type, a news event starts and the market response evolves as more news emerges and / or the story gets wider coverage. For these types of events, the span of dates for the news event may largely overlap with those of the market response.

The largest positive return anomaly for BA in the last six months occurred over a 5-day period from 3/8/2021 to 3/12/2021. The magnitude of the (beta-corrected) return anomaly was +16.4% and the total return for BA over this period was +20.6%. There were several news events over this period:

Three out of the four news events are related to increasing numbers of orders for planes and these are correctly identified as positive news in that the Act Event Score for each one is greater than 50. We selected the first of these news events, which is also the one with the most news articles, for the mapping table. In the other cases in the tables above, a single news event mapped to the return anomaly.

The largest negative return anomaly for the six month period ran from April 15th through April 21st. The corresponding news event occurred from April 16th through April 18th.

The market response to the development of this news story played out over 5 days, with the worst returns occurring towards the end of the period. The return for BA on the last day of the run is positive, but is lower than the beta-adjusted return expected relative to the S&P 500 (which is why this day is considered part of the negative return anomaly run). This is an intriguing example of a news-related market response that occurs over an extended period, such that investors had plenty of time to respond.

| Date | BA Price Return |

|---|---|

| 4/15/2021 | -0.52% |

| 4/16/2021 | -1.17% |

| 4/19/2021 | -1.62% |

| 4/20/2021 | -4.13% |

| 4/20/2021 | -4.13% |

| 4/21/2021 | 0.79% |

A number of the largest return anomalies for BA, both positive and negative, had no closely-corresponding news event. The 5th largest negative return anomaly is -5.81% and occurred on March 15th and 16th. Act’s analysis identifies no news events for BA over the period from March 14th to March 21st. This does not mean that there were no news stories on Boeing, but rather that none of the stories were consistently covering or expanding upon a common ESG theme.

Looking at the 10 largest positive and negative return anomalies with a matching news event, we calculated the average return anomaly, the average Act Event Score, and the average duration of the return anomalies. The average magnitudes of these return anomalies are substantial (+5.4% for positive anomalies, -4.5% for negative anomalies).

| Avg Return Anomaly | Avg Act Event Score | Avg Duration of Return Anomaly (Days) | |

|---|---|---|---|

| 10 Largest Positive Return Anomalies | 5.4% | 50.3 | 2 |

| 10 Largest Negative Return Anomalies | -4.5% | 40.7 | 3 |

The average Act Event Score leading or contemporaneous with a positive return anomaly is 50.3, as compared to 40.3 for a negative return anomaly. This result is consistent with the Act Event Score providing economically-material information in advance of positive and negative return anomalies for Boeing.

Summary

The application of machine learning to parse natural language text is advancing quickly, with exponential improvements in the power of underlying models in the last thirty six months. In finance, there is an enormous economic motivation to automate the process of reading news and determining if the news is potentially relevant to the share price. In this case study, our results suggest that the Act Analytics NLP and event aggregation may add value in identifying news events for BA that trigger significant share price responses and in determining whether the share price response is likely to be positive or negative.

Founded by former portfolio management, machine learning and market data experts, Act Analytics is leading the way for investment professionals to integrate accurate real time, independent ESG scores into their models. Act Analytics uses NLP sentiment analysis of 200+ trusted independent news sources, with tens of thousands of referenceable articles per day on 14,000+ entities to generate unique insights and transparency with 500,000+ real time equity scores for investors. For more information visit Act Analytics or reach out to info@act-analytics.com

Download PDF- Real time ESG intelligence

- 4 King St. West Suite 1060, Toronto, Ontario

- Tel +1 647 200 6482

- info@act-analytics.com