Case Study

Negative News Tipping Point for AstraZeneca Telegraphed Share Price Decline

Written by team at Act Analytics On May 19, 2021

11 min read

11 min read

AstraZeneca stock (AZN), along with stocks of other pharmaceutical companies producing COVID-19 vaccines, has experienced considerable volatility as the market incorporates emerging news. Along with the issues of vaccine efficacy, production, and distribution, there are complex questions relating to social equity, who bears vaccine costs, and intellectual property. AZN closed at $51.47 on June 12, 2020 and then rapidly rose 18.7% to close at $61.10 on July 17th. The gains in AZN’s share price were concentrated in just a few days, as AZN announced positive news relating to its COVID vaccine.

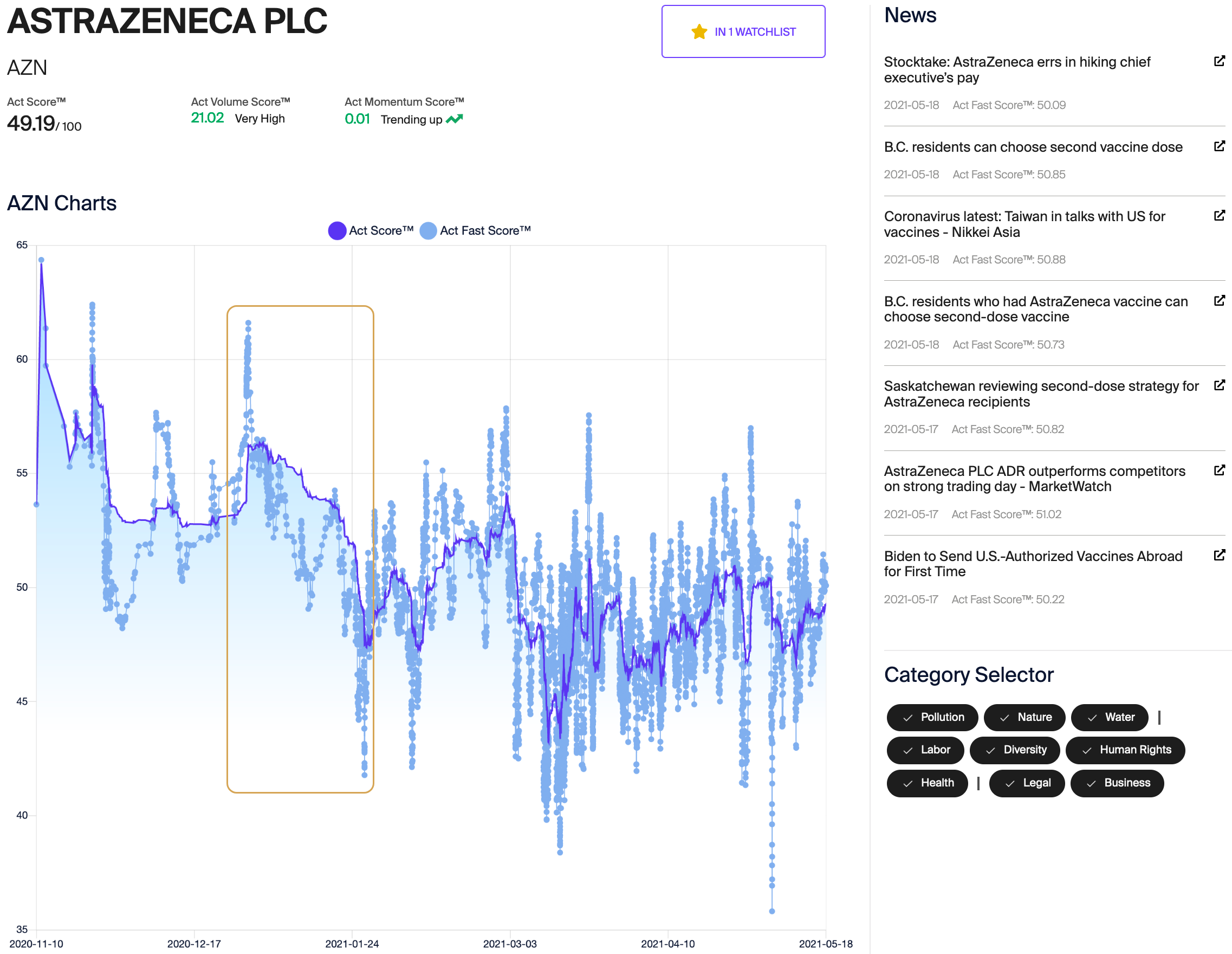

Today, AZN is trading at $55.26 and has not closed above $60 since the mid-July 2020 peak. The stock has closed as low as $47.23 in 2021 (on March 4th). AZN briefly closed above $58 on November 11, 2020, the closest it has come to regaining its mid-2020 high.

Because of the social and economic significance of COVID vaccines, as well as the complexity of the interplay of science, policy, and factors such as vaccine resistance, it is especially interesting to examine how the stock market adjusts share prices to reflect new information. We have identified some specific cases in which a series of news stories on one or more topics pertaining to a company lead substantial idiosyncratic multi-day moves in share prices. The Act Analytics scores, which determine whether emerging news is positive or controversial on a range of social and economic measures, provide a standardized objective basis for aggregating new information. While users can choose which classes of issues to screen for, our case studies screen on the complete set of nine categories in the Act Analytics system (below).

The Act Analytics system analyzes each news story that mentions AZN and pertains to any of these categories and determines whether the news is positive or negative for the company. The Act Score is the aggregate of the most-recent 200 news stories and the Act Fast Score is calculated based on the most-recent 25 news stories.

In this case study, we have analyzed an extended decline in AZN’s Act Scores starting at the beginning of 2021. After AZN’s Act Score and Act Fast Score peaked on 12/30/2021, both scores declined through January, reaching minimums on 1/27/2021. This was a substantial and persistent fall, with the Act Fast Score going from 61.6 on 12/30/2021 to 41.78 on 1/27/2021. The news that drove the decline in the Act Score related to the firm’s COVID-19 vaccine and included reports of uncertainty relating to vaccine dosing, distribution issues, and political issues.

To determine whether there are meaningful runs in AZN’s share price relative to the score decline, we have analyzed AZN against the S&P 500 (using the ETF SPY), the global market-cap-weighted equity index (using the ETF VT) and two ETFs that focus on pharmaceuticals and biotech and have substantial AZN holdings1: VanEck Vectors Pharmaceutical ETF (PPH) and the iShares Nasdaq Biotechnology ETF (IBB).

We have determined the largest anomalous runs of returns for AZN relative to these four benchmarks over the last six months (through May 12th). The single largest run in negative returns for AZN relative to SPY started on January 27th and ended on February 3rd. There are also anomalous return runs in AZN relative to these other benchmarks over the same period.

| Benchmark | Run Start | Run End | AZN Price Return | Benchmark Price Return |

|---|---|---|---|---|

| S&P 500 (SPY) | 1/27/2021 | 2/3/2021 | -8.16% | -0.51% |

| VT | 1/27/2021 | 2/3/2021 | -8.16% | -0.38% |

| PPH | 1/27/2021 | 2/3/2021 | -8.16% | -2.75% |

| IBB | 1/27/2021 | 2/3/2021 | -8.16% | -0.58% |

For all of these benchmarks, the run of anomalous daily negative returns lasted six consecutive trading days. Using SPY and VT as the benchmarks, this anomalous negative return sequence was the largest in the six-month period. With IBB as the benchmark, this was the second-largest anomalous return sequence for the period. When PPH was used as the benchmark, this was the fourth-largest return anomaly sequence for the six-month period. In all cases, AZN’s negative return over this period was large compared to the benchmarks.

A notable feature of this case study is that the Act Scores for AstraZeneca declined fairly continuously over most of January, but the major anomalous price decline for the stock started on January 27th, the day that the Act Fast Score reached its minimum. Rather than having the share price decline incrementally as negative news emerged, the market did not react until some critical threshold in sentiment was reached. Once the sell-off triggered, AZN experienced six subsequent anomalous down days. The sequence of events suggests that perhaps emerging news has a cumulative effect and that the market does not respond until a critical tipping point in sentiment is reached.

There is another extended and substantial drop in Act Scores from March 2nd to March 15th, but there is no large-magnitude anomalous return during or subsequent to this period. The news was less uniformly negative during this decline, however, as evidenced by much higher levels of high-frequency / short-term spikes, both up and down, in the Act Fast Score. During the January decline in Act Scores, the Act Fast Score is below the standard Act Score for the vast majority of the period. During the March decline, the Act Fast Score is frequently above the standard Act Score. Perhaps a mix of positive and negative news for a company mutes the market’s response even though the prevailing trend in sentiment is downward.

As we examine extended runs of price return anomalies that occur near a large move in sentiment, as measured with Act Scores, we are trying to understand how the market processes news events. In this case, the news related to AstraZeneca’s COVID-19 vaccine, but the stories covered various aspects of the challenges facing the company. AZN’s notable early-February decline, following an extended period of bad news on multiple topics, is an interesting case. This period exhibited a substantial volume of stories that were consistently negative, such that the Act Fast Score spent most of January below the slower-changing Act Score. We plan to seek out similar cases for other companies to determine whether similar evolutions in sentiment will also presage major market movements. The concept of a tipping point in overall sentiment, beyond which the market responds, is intriguing and consistent with research on tipping points in news coverage.

Download PDF- Real time ESG intelligence

- 4 King St. West Suite 1060, Toronto, Ontario

- Tel +1 647 200 6482

- info@act-analytics.com