Case Study

Building Negative Sentiment Due to Apple Antitrust Investigations Leads Share Price Decline

Written by team at Act Analytics On May 16, 2021

12 min read

12 min read

As we analyze large real time changes in Act Analytics’ news-based ESG sentiment scores for stocks, we identify cases that merit exploration. While it is natural to assume that the market responds extremely fast to emerging news, we see cases--even with high-profile companies--in which the market appears to take significant periods of time to process the significance of events as the news unfolds. We examine these events using Act Analytics’ ESG Sentiment Scores which uses Natural Language Processing (NLP) to diagnose trusted independent media stories as being positive or negative on a stock.

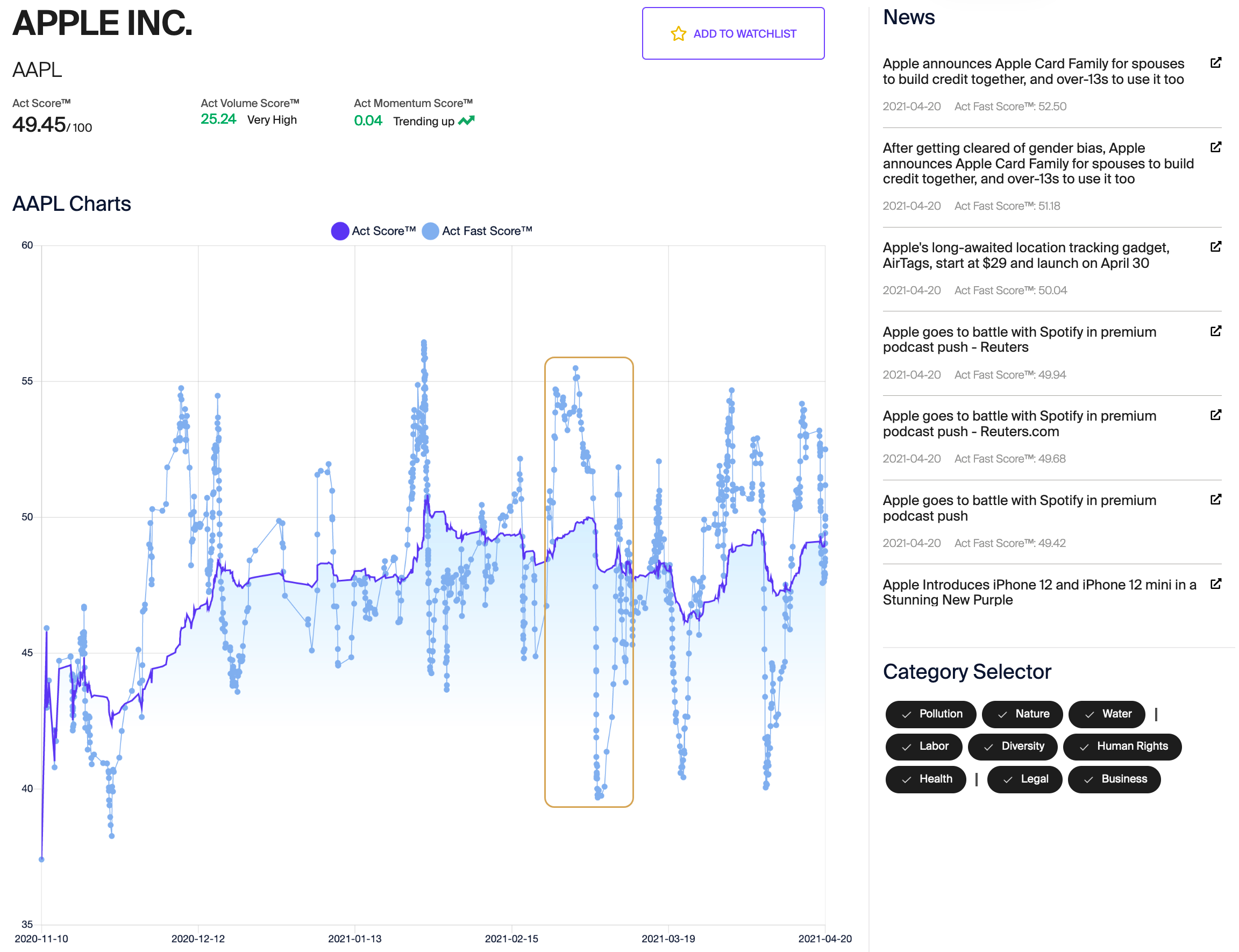

For the 5-month period from November 20, 2020 to April 20, 2021, the Act Fast Score for Apple (AAPL) has varied from a low of 38.2 to a high of 56.4. Over one 6-day period, from February 28th, 2020 to March 4th, 2020, the Fast Score fell from 55.49 to 39.68, spanning almost the entire 151-day range. This rapid large-magnitude decline in the Act Fast Score started with the passage of a bill in the Arizona House that limits Apple’s ability to control billing for App Store purchases. This was followed by the announcement of antitrust cases against Apple in Europe. As more news became available in the U.K. and E.U. antitrust situation, the sentiment score fell dramatically over the 6-day period.

1. The Act Fast Score calculates sentiment using the weighted-average of the sentiment calculated for the most-recently published 25 articles for a stock, with more recent articles receiving higher weights.

Given the magnitude of the sentiment impacts of the AAPL news, we have examined the extent to which this negative news has impacted the stock price. We calculated and ranked stock-specific return runs for Apple over the 120 days through 4/20/2021. Calculating a return run starts by computing the stock’s return anomaly for each day, the difference between the price return on the stock and the expected return based on the stock’s beta and the return of the market index for that day. The return anomalies are then compounded over a run of successive days of either negative or positive anomalies. For details on this procedure, please see the overview document.

| Positive Run | End Date | Negative Run | End Date |

|---|---|---|---|

| 0.16% | 3/11/2021 | -0.74% | 4/16/2021 |

| 0.22% | 3/29/2021 | -0.83% | 12/23/2020 |

| 0.23% | 1/5/2021 | -0.84% | 3/30/2021 |

| 0.23% | 3/4/2021 | -0.89% | 4/1/2021 |

| 0.30% | 4/15/2021 | -0.96% | 3/12/2021 |

| 0.38% | 2/19/2021 | -1.28% | 4/14/2021 |

| 0.91% | 2/4/2021 | -1.38% | 4/12/2021 |

| 1.23% | 4/19/2021 | -1.44% | 3/3/2021 |

| 1.23% | 1/13/2021 | -1.50% | 1/12/2021 |

| 1.26% | 1/8/2021 | -1.83% | 3/10/2021 |

| 1.28% | 3/31/2021 | -1.90% | 1/19/2021 |

| 1.97% | 3/9/2021 | -2.39% | 3/18/2021 |

| 2.00% | 4/13/2021 | -3.48% | 3/26/2021 |

| 2.44% | 3/23/2021 | -4.04% | 1/4/2021 |

| 2.52% | 12/28/2020 | -4.11% | 2/24/2021 |

| 2.88% | 3/1/2021 | -4.24% | 1/6/2021 |

| 3.05% | 3/16/2021 | -5.01% | 3/8/2021 |

| 4.00% | 4/9/2021 | -7.20% | 2/18/2021 |

| 12.93% | 1/27/2021 | -8.45% | 2/3/2021 |

The left side of this table shows the ranked positive return anomalies and the right side shows the negative return anomalies. There is a 2-trading day negative return run of -5.01% that ends on 3/8/2021. This is the 3rd largest-magnitude negative run over the 120-day period. The first day of the decline was Friday, March 5th, and the decline continued on Monday, March 8th. Over this 2-trading day period, AAPL’s price return was -3.1% vs. +1.3 for the S&P 500.

What is particularly intriguing about this case is that there was an extended decline in sentiment over 6 days before the stock-specific decline began. There was a multi-day period of substantially-falling sentiment before the market responded to the news.

It is also notable that the sentiment score declined over multiple days with the publication of more news stories pertaining to alleged anticompetitive practices. In many other cases, a large change in sentiment rating is due to a succession of positive or negative news events, as opposed to amplification of one story as we see here. A cascade of different news stories which reinforce a sentiment trend will also be of interest, but we chose this specific case because of the extended trend associated with multiple news stories on a single issue.

This case, and similar cases, has potentially important implications for how the capital markets respond to emerging news. An extended period between when the news emerges and when the market responds provides opportunities for investors. For ESG-oriented investors, responding quickly to relevant news may be important in capturing potential upsides associated with responsible investing.

Case studies are, by their very nature, anecdotal. Even as we acknowledge the limitations in looking at specific events, we hope that readers will find them interesting in thinking about how automated real-time calculations of sentiment on relevant investing criteria may be useful. For more case studies, white papers and updates, visit us online at www.act-analytics.com.

Download PDF- Real time ESG intelligence

- 4 King St. West Suite 1060, Toronto, Ontario

- Tel +1 647 200 6482

- info@act-analytics.com