Blog

Risk Reduction with ESG

Written by team at Act Analytics On Nov 2, 2020

8 min read

8 min read

Introduction

ESG has seen an explosion of interest in recent years. Money is flowing into ESG strategies like never before. Investors want to understand ESG’s impact on risk. Are there tradeoffs? This is an area of ongoing discussion; no consensus has been reached. We’re motivated to contribute to this discussion through data driven arguments.

We demonstrate that higher Act Analytics ESG scores correlate with lower Riskalyze risk numbers for public companies on the NYSE, even after adjusting for company size. This suggests that companies who choose to focus on ESG tend to also be less risky as investment decisions.

ESG and Risk

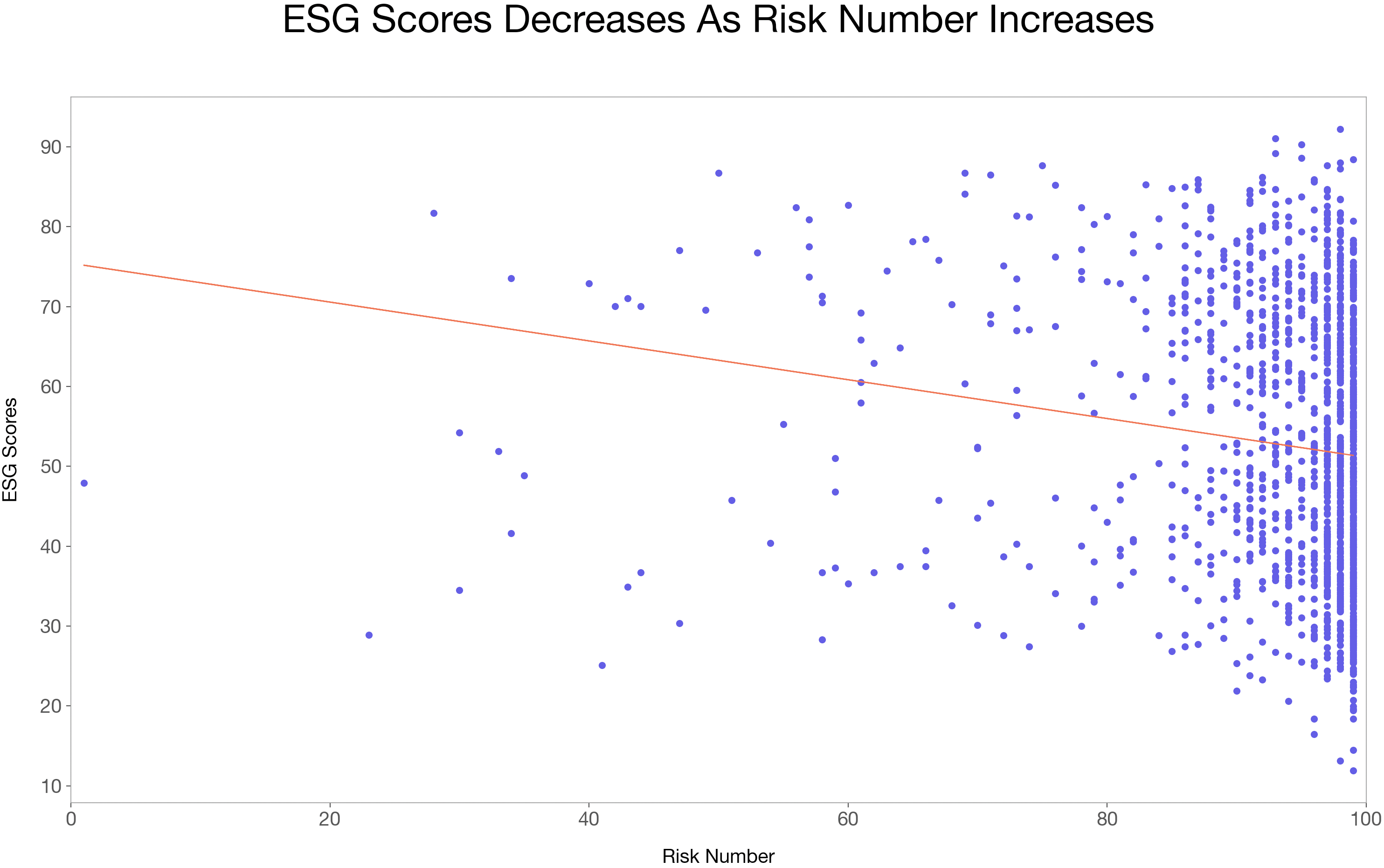

First, we explore the relationship between the Act Analytics ESG score and the Riskalyze Risk Number by means of correlation.

Figure 1 plots ESG score and Risk Number for companies on the NYSE. We include a red regression line to help demonstrate the relationship:

This already gives us interesting insights. ESG score and Risk Number are negatively correlated 0.148. Companies with higher ESG scores tend to have lower Risk Numbers. To be clear, a lower risk number means less risk.

There’s more to say. Now we dig deeper to understand how durable the relationship is.

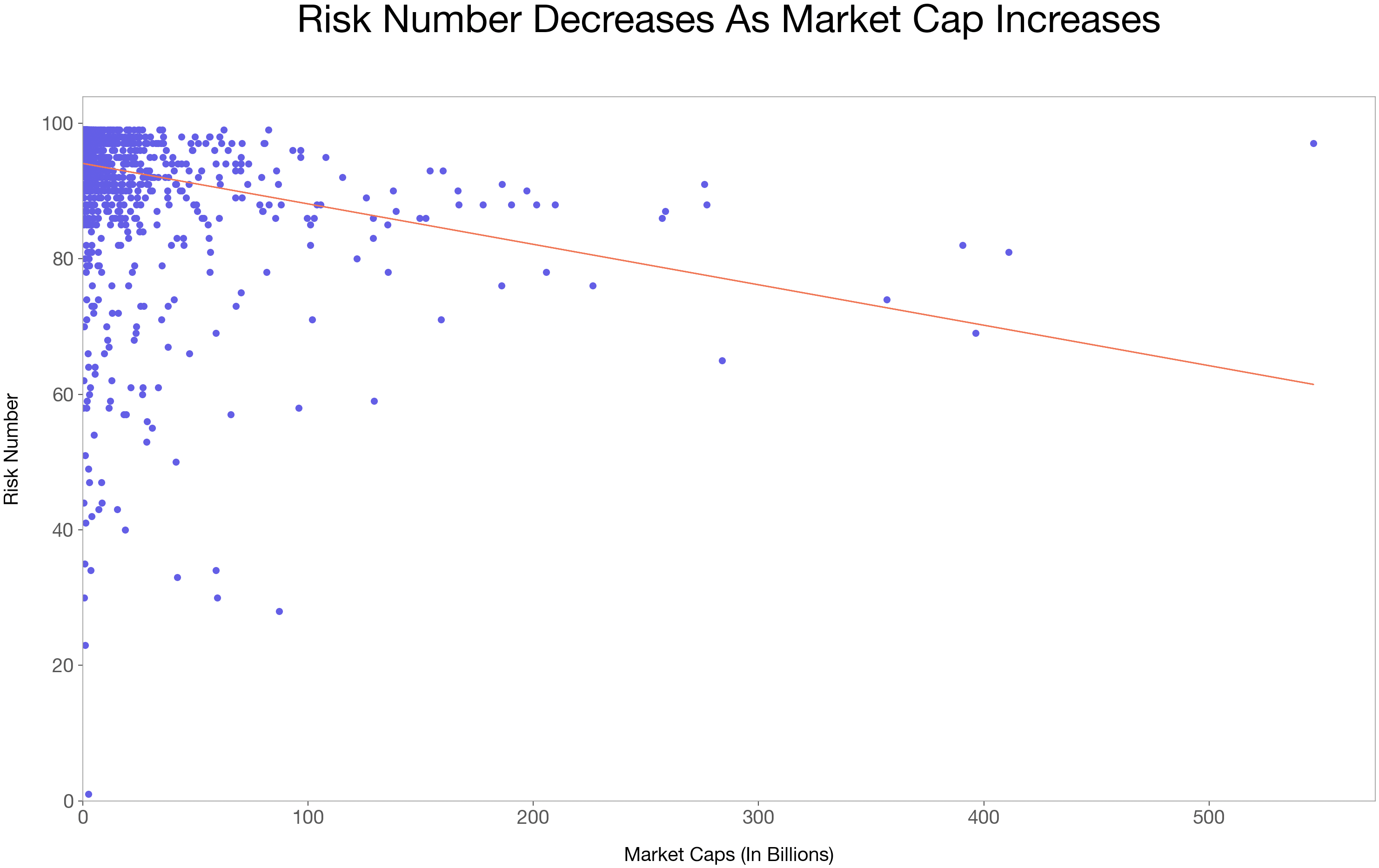

Size Bias

The Act Analytics ESG score includes company disclosures of ESG metrics. This leads to a size bias. We expect larger companies to tend to be less risky investments, so we expect some size bias in the risk number as well.

Figure 2 demonstrates a size bias in both the ESG score and the risk number:

This calls into question the strength of our first result. Of course two size biased factors are correlated, that’s not a very inspirational result.

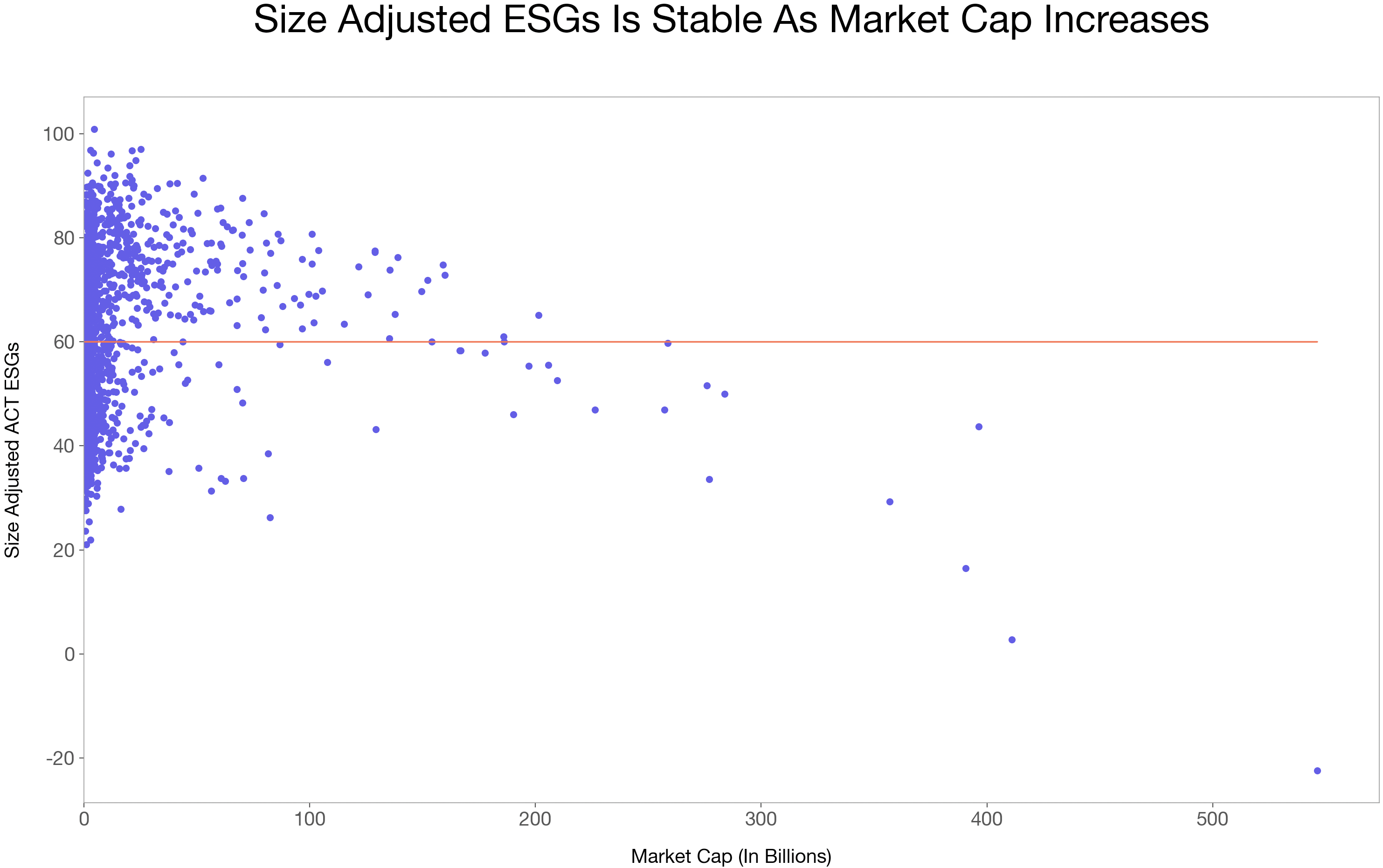

Adjusting for Size Bias

We compute the portion of the ESG score and Risk Number not explained by the size biases.

To do this, we regress ESG score to market cap:

ESG_Score = β × Market_Cap + α

The difference between the ESG_Score and the regression is our size adjusted ESG score.

Size_Adj_ESG_Score = ESG_Score − β × Market_Cap − α

We perform a similar operation on the Riskalyze Risk Number.

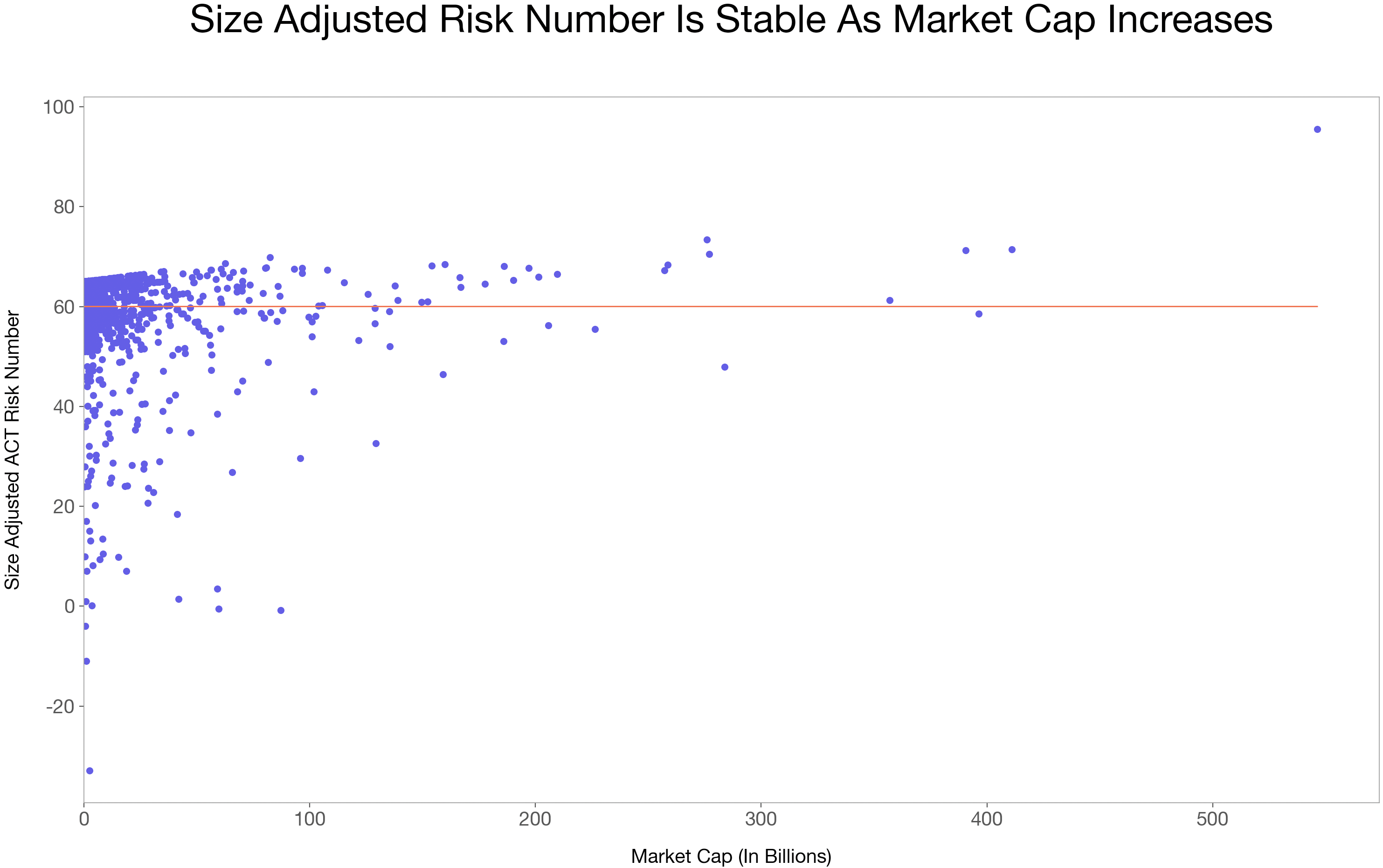

Figure 3 demonstrates these transformations:

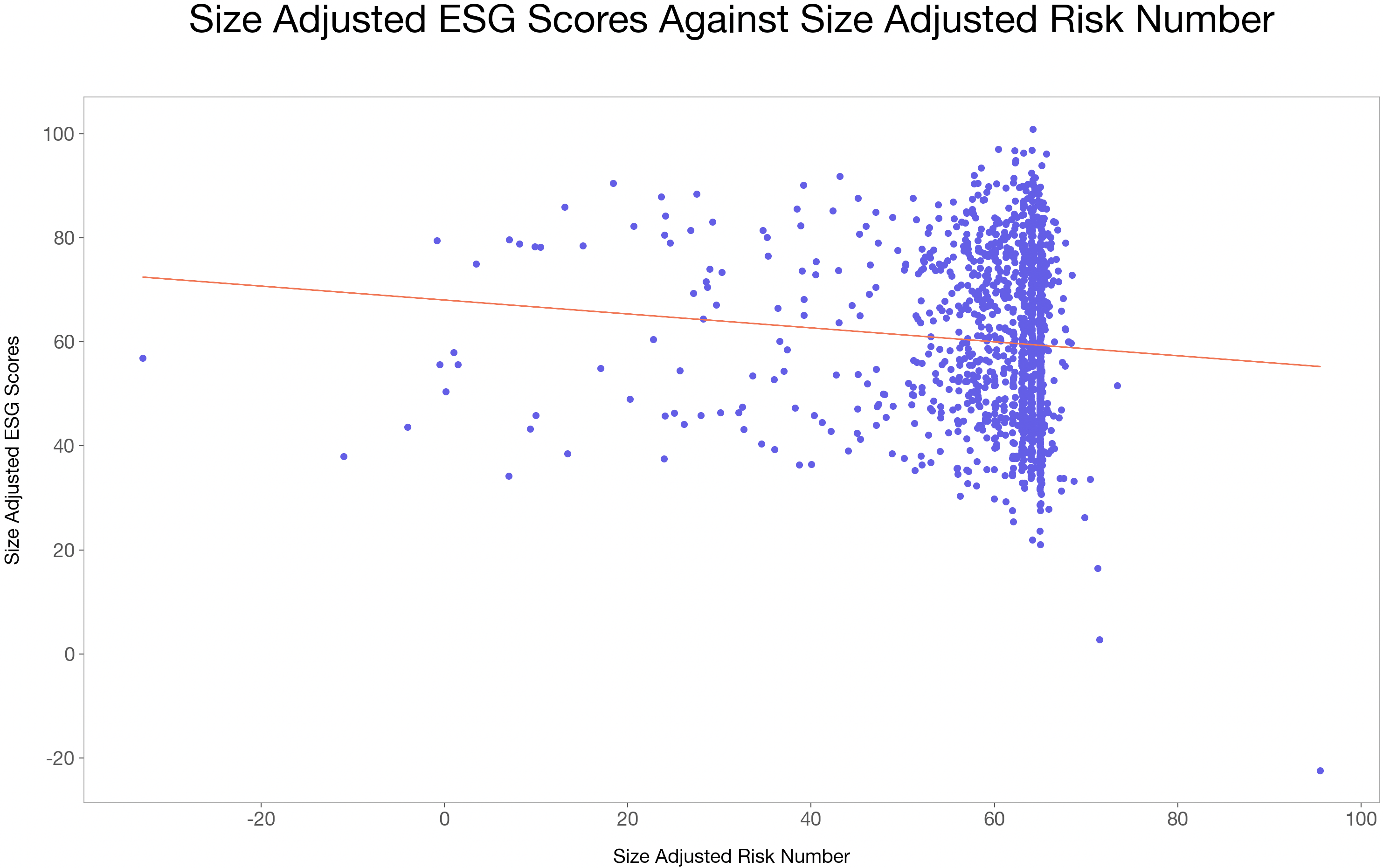

Finally, Figure 4 compares the size adjusted Act Analytics ESG score and size adjusted Riskalyze Risk Number:

We see a negative correlation -0.083 between the size adjusted Act Analytics ESG score and size adjusted Riskalyze Risk Number.

Higher ESG scores correlate with lower risk numbers for public companies on the NYSE, even after adjusting for company size. This suggests a more powerful relationship than we initially anticipated. If we saw no correlation after size adjustments, that would have still been an encouraging result. This result leads us to double down on our position that including ESG in the investment process reduces risk.

- Real time ESG intelligence

- 4 King St. West Suite 1060, Toronto, Ontario

- Tel +1 647 200 6482

- info@act-analytics.com