Blog

Act Analytics Method Overview

Written by team at Act Analytics On May 4, 2021

10 min read

10 min read

Introduction

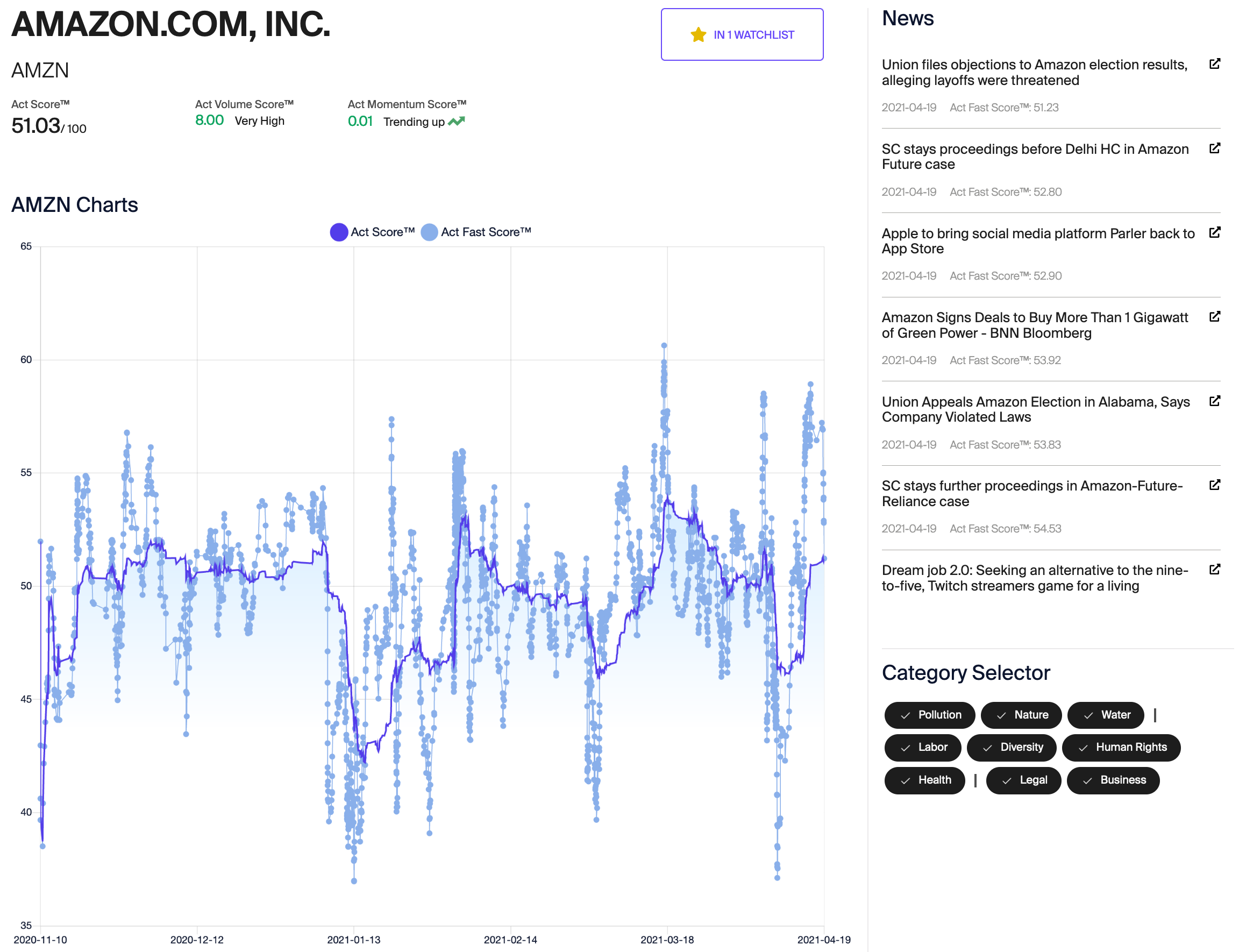

Act Analytics uses machine learning to generate news-driven ESG sentiment ratings for stocks that evolve in real time, as new information becomes available. Stocks are rated on the basis of a user-defined universe of themes. The ratings are generated using Natural Language Processing (NLP) analysis of trusted, independent news about a company. The NLP algorithms diagnose whether news is positive or negative and adjust the scores accordingly. In particular, there is the Act Fast Score that reacts quickly to news and the standard Act Score score that highlights longer-term trends.

One of the primary applications of the Act Score is for generating customized SRI/ESG ratings. The Category Selector function allows users to create their own tailored ratings based on the criteria they select. In the example above, for Amazon, the categories used to rate the stock are listed.

Each point on the Fast Score line represents a news item and users can hover over each item to see the title. Clicking on the news item pulls up the supporting article.

Qualitative Analysis Procedure

An important question about news-driven scores is how the market reacts to changes in scores. The market price of a stock is the net present value of the estimated future earnings stream. Bad news tends to reduce the earnings outlook and thereby reduces the current fair price. There tends to be some lag time between the emergence of bad news and when the market processes the implications of the news on the outlook for a company. We are starting to generate a library of case studies of substantial ESG news-driven changes in the Act Scores and how the market appears to adjust stock prices to reflect the news.

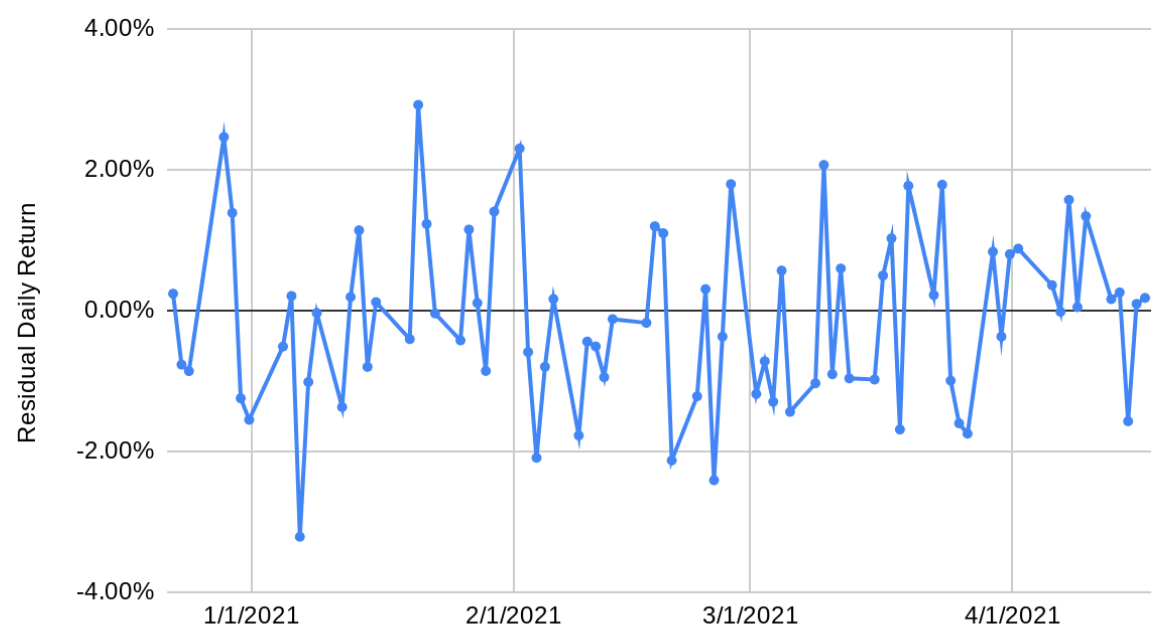

Our goal is to identify how company-specific news is processed by the market. To begin, we have to identify periods of significant gain or loss in the stock price that is independent of the returns in the market as a whole. To accomplish this, we subtract the component of a stock’s return that is attributable to the market. What remains is what is referred to as the residual in the CAPM model. We are analyzing short periods of time, so we approximate the CAPM in the following form (ignoring variability in the risk-free rate of return) and use daily return.

Return of a Stock = beta * (Return of the Market) + Residual

The time series of the residuals is where we start our analysis. Using the example of Amazon (AMZN), here is the residual return series for the last 120 days:

In this case, we have used the S&P 500 as the market index.

We are interested in large 1-day residual returns but we are even more interested in consistent negative or positive runs of residuals that suggest a consistent response to some outside news.

| Positive Run | End Date | Negative Run | End Date |

|---|---|---|---|

| 0.12% | 1/15/2021 | -0.02% | 4/6/2021 |

| 0.17% | 2/5/2021 | -0.37% | 3/30/2021 |

| 0.21% | 1/5/2021 | -0.40% | 1/19/2021 |

| 0.28% | 4/16/2021 | -0.46% | 1/25/2021 |

| 0.31% | 2/23/2021 | -0.80% | 1/14/2021 |

| 0.57% | 3/4/2021 | -0.86% | 1/28/2021 |

| 0.60% | 3/11/2021 | -0.90% | 3/10/2021 |

| 0.84% | 3/29/2021 | -1.57% | 4/14/2021 |

| 1.26% | 1/27/2021 | -1.62% | 12/24/2020 |

| 1.34% | 1/13/2021 | -1.69% | 3/18/2021 |

| 1.53% | 3/17/2021 | -1.93% | 3/15/2021 |

| 1.80% | 2/26/2021 | -2.46% | 3/8/2021 |

| 2.06% | 4/5/2021 | -2.77% | 2/25/2021 |

| 2.07% | 3/9/2021 | -3.16% | 3/3/2021 |

| 2.31% | 2/18/2021 | -3.27% | 1/4/2021 |

| 3.43% | 4/13/2021 | -3.32% | 2/22/2021 |

| 3.74% | 2/1/2021 | -3.44% | 2/4/2021 |

| 3.82% | 3/23/2021 | -3.90% | 2/16/2021 |

| 3.89% | 12/29/2020 | -4.28% | 3/26/2021 |

| 4.19% | 1/21/2021 | -5.54% | 1/11/2021 |

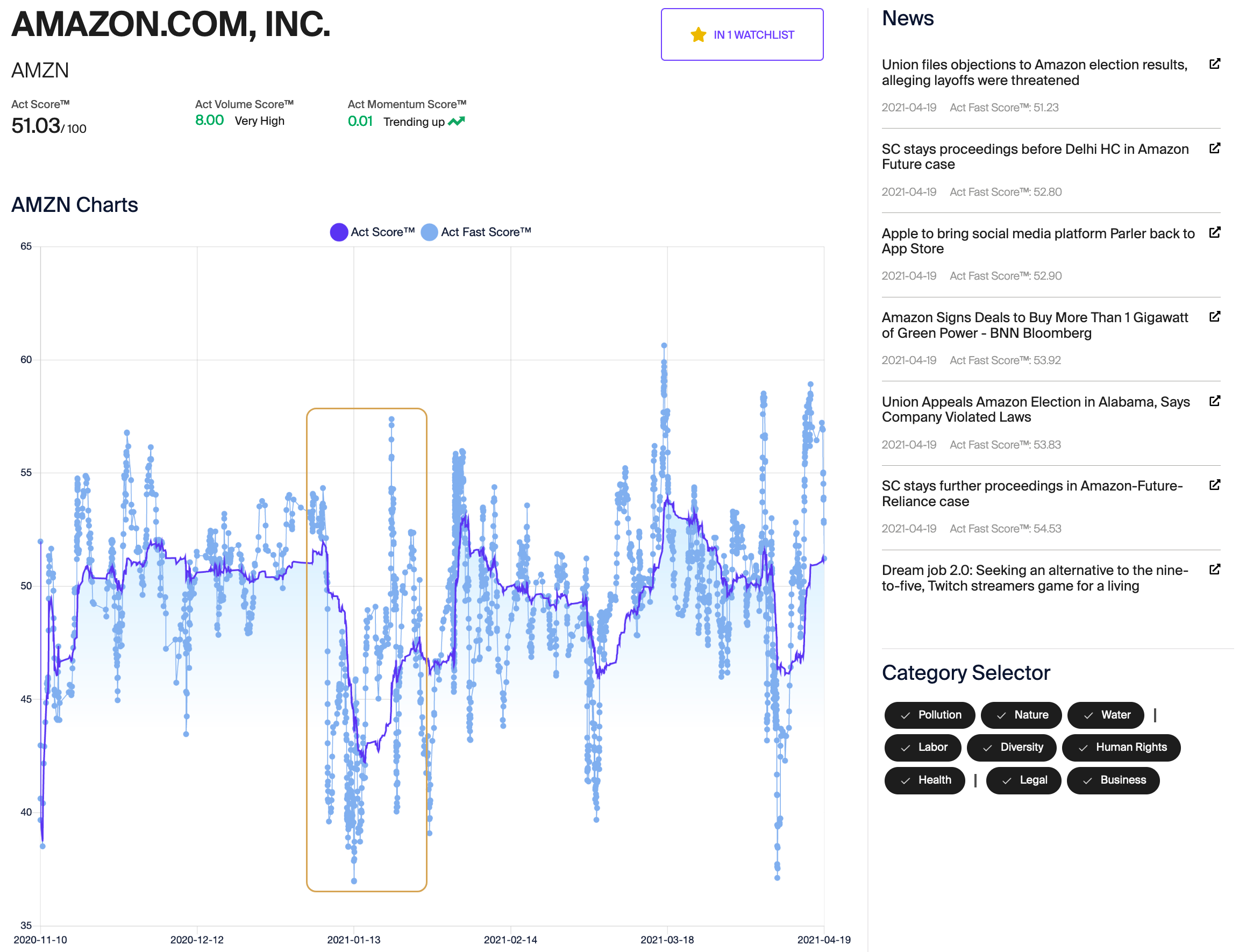

There was a substantial drop in the Act Score, starting on about January 6th (peak Fast Score=54.34) and ending on about January 15th (Fast Score=42.11). There is a consistent and steady decline in the Act Score over this period. Looking back at the residual runs table, the most significant residual run over the past 120 days ended on January 11th and the magnitude is -5.54%. This decline occurred over 4 trading days, starting on January 6th. AMZN returned -4.92% relative to the S&P 500 over this 4-day period.

After January 15th, the Act Score trends upwards and rises rapidly, with the Fast Score reaching a peak of 57.29 on January 20th. The largest residual return run for AMZN over the past 120 days is 4.19%, ending on January 21. This run took place over two days: January 20 and January 21. AMZN returned +4.5% relative to the S&P 500 over this 2-day period.

Summary

We will be using the procedure used in the AMZN example to identify cases in which a substantial change in the Act Score precedes a significant return anomaly for a stock. For this example, a large peak-to-trough-to-peak change in the Act Score corresponds to a subsequent decline in AMZN relative to the overall market, followed by a rebound relative to the overall market. In this case, it is intriguing that the changes in the Act Score occur well before the news is reflected in changes in the stock prices.

- Real time ESG intelligence

- 4 King St. West Suite 1060, Toronto, Ontario

- Tel +1 647 200 6482

- info@act-analytics.com